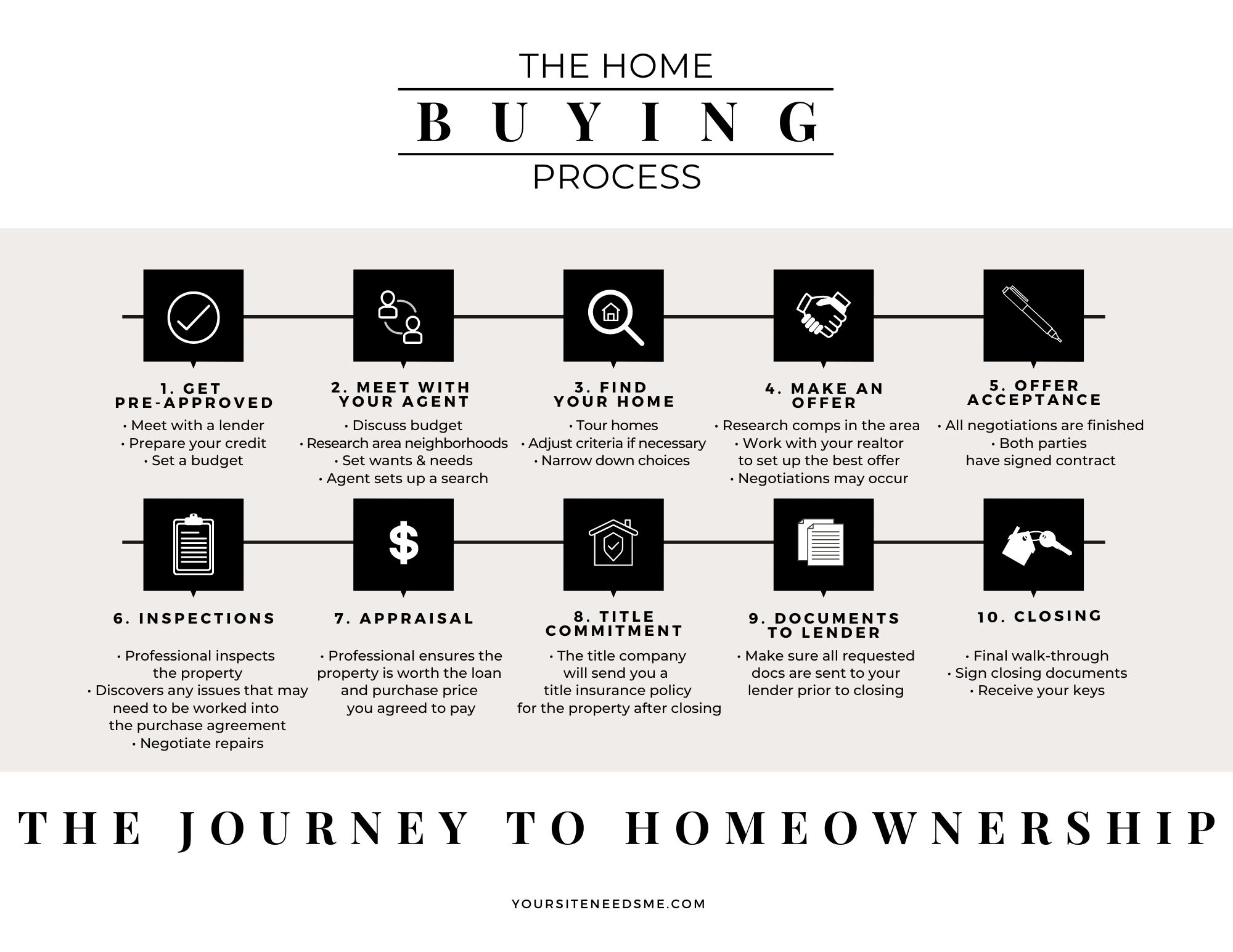

Investing in a Vacation Property? Learn What You’ll Need to Have to Get A Mortgage Approved

With approximately one million people having purchased vacation homes in the last year, this type of residence is gaining popularity for those who are interested in a home in a beach setting or a vacation hot spot. However, while a second home can seem like a great purchase and solid investment opportunity, there are different requirements that go into this type of purchase. If you’re considering a vacation home, you may want to be aware of the following financial factors.

With approximately one million people having purchased vacation homes in the last year, this type of residence is gaining popularity for those who are interested in a home in a beach setting or a vacation hot spot. However, while a second home can seem like a great purchase and solid investment opportunity, there are different requirements that go into this type of purchase. If you’re considering a vacation home, you may want to be aware of the following financial factors.

The Down Payment Amount

If you currently have a primary residence, you may be aware that you don’t need to put down 20% or even 10% in order to make a home purchase, but things are different when it comes to a vacation home. Because you will be taking on an additional mortgage, there is greater risk involved, and this means you will likely have to put in at least 10 percent. Because of this, many homebuyers utilize the equity they have in their first home to make up the down payment.

About The Credit Score

Most people that have a credit score of more than 500 have the ability to use a mortgage product and purchase a home, but if you’re buying a second property, you’ll need a higher credit score in order to facilitate the purchase. Because there is more risk involved, lenders will want to make sure you’re a good bet. In addition, if you do have a lower credit score, lenders like Fannie Mae may also expect you to put more down to decrease the risk involved for them.

The Income Required

Since you’ve been through the mortgage process for your first home, you’re probably aware that you debt-to-income (DTI) ratio needs to be a certain amount in order to qualify for a mortgage. While your DTI for a primary residence may be a little bit higher since it’s your only payment, this ratio will be lower for your vacation home since it’s higher risk. This means you’ll require a slightly higher income than for your primary residence in order to get approved.

Deciding to purchase a vacation home can be a very exciting concept for many people, but there are a number of different financial requirements that go along with buying another residence. If you’re in the market for a vacation property and are curious about what’s involved, contact your local real estate professional for more information.