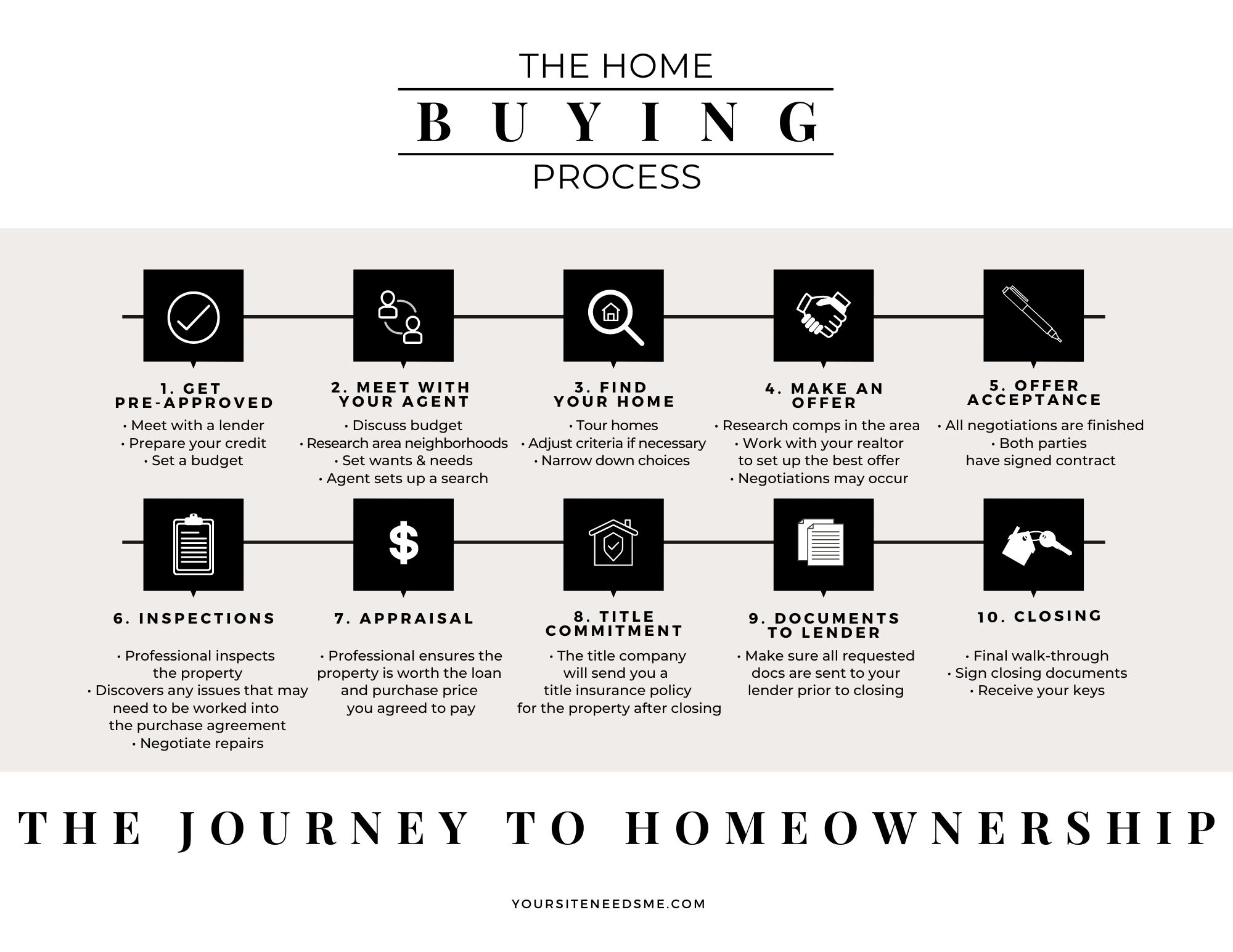

The 5-Minute Guide To Flood Insurance: What It Is, How It Works, And Whether You Need It

You’ve got house insurance, and assume your property is covered for any type of detrimental occurrence that can possibly take place.

You’ve got house insurance, and assume your property is covered for any type of detrimental occurrence that can possibly take place.

However, not all homeowners are aware that home insurance policies don’t necessarily cover damage related to a flood, as the risks are too great. As a result, homeowners must purchase flood insurance through a private company.

Floods are one of the most common hazards in the US, costing billions of dollars in damage to properties every year.

Since this is a common issue lately, the federal government updating these policies currently so please talk with your real estate professional or local insurance company for the most up to date information.

What Is Flood Insurance?

Flood insurance policies are typically made available to homeowners in flood-prone areas. The majority of insurance policies cover some form of water damage, from things like leaking faucets to bursting plumbing pipes.

However, such policies don’t cover water damage as a result of flooding of rivers or sewers that cause water to ruin a home.

Specific flood protection is provided by the National Flood Insurance Program (NFIP), which is run by the Federal Emergency Management Agency (FEMA). Standard flood insurance policies cover “direct physical damage” to a property resulting from floods.

A separate policy must be purchased to protect the belongings inside the home or building. Homeowners can buy up to $250,000 in coverage for the home, and up to $100,000 in coverage for possessions. Even renters are permitted to purchase flood insurance to cover their possessions.

How Does Flood Insurance Work?

Flood insurance isn’t sold by FEMA directly, but rather is sold to customers through private insurance agencies. Premium rates are determined by the government, and they remain consistent from one insurer to the next.

How much a homeowner pays for their own specific flood insurance depends on a number of factors, including how prone the neighborhood is to floods and how much coverage a homeowner wants. The average annual premium is approximately $520 for $100,000 worth of coverage for a property with no basement, and approximately $615 annually for a property with a basement.

Filing A Flood Insurance Claim

The claims process is like any other insurance claim. Once the claim is filed, the damage will be analyzed by an adjustor assigned by the insurance company. A “proof of loss” form will need to filled out and submitted to the insurer within 60 days of the flood occurrence.

Do You Need Flood Insurance?

It’s necessary to find out if you are eligible for flood insurance before buying it. For residents of a community to be eligible, the community needs to enforce floodplain statutes to lessen the chances of flood damage, after which FEMA ensures that such regulations are followed.

Only those who reside in a community that participates in NFIP can buy insurance – today, about 20,000 communities across the country participate in this program.

FEMA offers maps that outline what areas are at high risk for floods, and those that are at moderate-to-low risk. The law requires homeowners to have flood insurance if the properties are located in a high-risk zone and have a federally-backed mortgage. This is because properties located in these high-risk areas have a 26 percent chance of suffering flood damage during the 30 years that it would take to pay off a mortgage.

Homeowners are not required to buy flood insurance if they reside in a moderate-to-low-risk zone, though it may be a good idea to purchase it anyway. Properties outside the high-risk areas make up over 20 percent of NFIP claims. Homeowners in these areas can purchase up to $200,000 in flood insurance.

The bottom line is, even if you don’t necessarily live in a high-risk zone, this doesn’t mean your home won’t ever get flooded. Many conditions can result in flood damage, including clogged drain systems, flash rainstorms, and damaged levees.